A list of open funding opportunities:

| Call Ref: | Topic | Type of action |

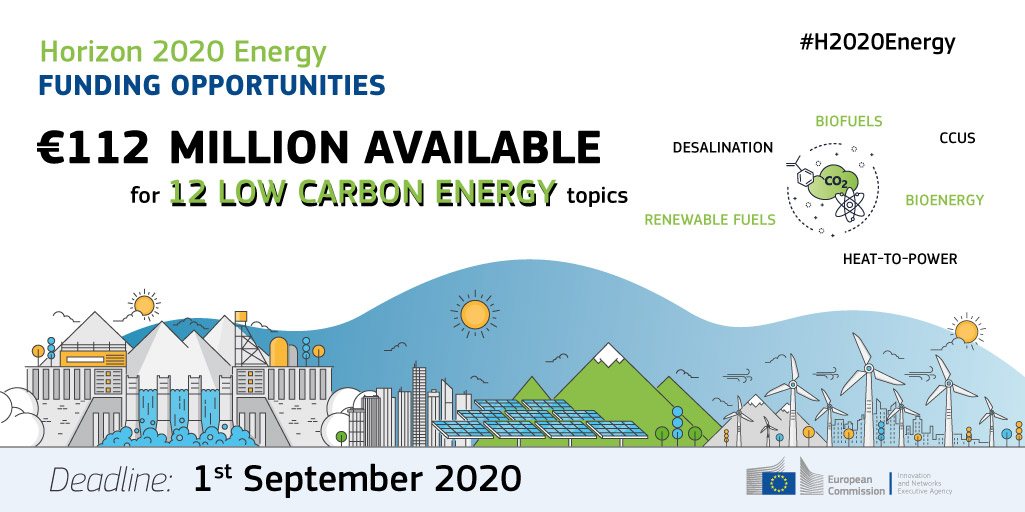

| LC-SC3-NZE-6-2020 | Geological Storage Pilots | RIA |

| LC-SC3-CC-1-2018-2019-2020 | Social Sciences and Humanities (SSH) aspects of the Clean-Energy Transition | RIA |

| LC-SC3-CC-7-2020 | European Energy and Climate Modelling Forum (2020-2024) | RIA |

| LC-SC3-RES-20-2020 | Efficient combination of Concentrated Solar Power and desalination (with particular focus on the Gulf Cooperation Council (GCC) region) | IA |

| LC-SC3-RES-34-2020 | Demonstration of innovative and sustainable hydropower solutions targeting unexplored small-scale hydropower potential in Central Asia | IA |

| LC-SC3-RES-3-2020 | International Cooperation with USA and/or China on alternative renewable fuels from sunlight for energy, transport and chemical storage | RIA |

| LC-SC3-RES-25-2020 | International cooperation for Research and Innovation on advanced biofuels and alternative renewable fuels | RIA |

| LC-SC3-RES-36-2020 | International cooperation with Canada on advanced biofuels and bioenergy | RIA |

| LC-SC3-ES-13-2020 | Integrated local energy systems (Energy islands): International cooperation with India | IA |

| LC-SC3-SCC-2-2020 | Positive Energy Districts and Neighbourhoods for urban energy transitions | ERANET |

| LC-SC3-CC-9-2020 | Industrial (Waste) Heat-to-Power conversion | IA |

| LC-SC3-NZE-5-2020 | Low carbon industrial production using CCUS | IA |

Source: www.kpk.gov.pl

As a basic rule, to be eligible, costs must be:

Actual and incurred by the beneficiary

Incurred during the project duration (except for costs of the final report)

Indicated in the estimated budget in Annex 2 (budget of the action)

Incurred in connection with the action as described in Annex 1 (proposal description)

Reasonable and justified, and compliant with the principle of sound financial management

Identifiable and verifiable, in particular recorded in the beneficiary’s account (according to

accounting standards of the beneficiary’s country and to usual cost accounting practices).

Five cost categories are considered:

A. Direct personnel costs

B. Direct costs of subcontracting

C. Costs of providing financial support to third parties

D. Other direct costs

Travel costs and related subsistence allowances

Depreciation costs of equipment, infrastructure and assets or costs of renting and

leasing equipment, infrastructure and assets (see also Q 3.1.6)

Costs of other goods and services (see also Q 3.1.7)

Capitalised and operating costs of large research infrastructure (see also Q 3.1.8)

E. Indirect costs

National Contact Point:

Aneta Maszewska

tel.: +48 508 101 008, +48 22 828 74 83

e-mail: Aneta.Maszewska@kpk.gov.pl

Maria Śmietanka

tel.: +48 502 052 239, +48 22 828 74 83

e-mail: Maria.Smietanka@kpk.gov.pl

International Cooperation Center:

tel: 81 537 54 58/54 98

e-mail: cwm@umcs.pl